May 2026 Round Up

A lot is landing on 1 July 2026. Payday Super starts, the new anti-money laundering rules kick in for accountants, and the ATO is sharpening its focus on holiday home deductions for this tax time. We’ve covered what each one means for you below.

We’ve also pulled out the five proposed changes from the 2026-27 Federal Budget most likely to affect investors, business owners and trust holders, and looked at why personal risk insurance premiums are rising across every cover type.

1. What Employers Need to Do Before Payday Super Starts on 1 July 2026 Read the full article

2. Personal Risk Insurance Premiums Are Rising: Here’s Why Read the full article

3. Will the New Anti-Money Laundering Rules Affect You from 1 July 2026? Read the full article

4. Renting Out Your Holiday Home? New ATO Rules Could Deny Your Deductions Read the full article

5. 2026-27 Federal Budget: The Changes Most Likely to Affect You Read the full article

Payday Super: preparing your payroll system for July

From 1 July 2026, employers must pay super guarantee on every payday instead of quarterly. With less than two months to go, the time to prepare your payroll, cash flow and processes is now.

From 1 July 2026 super must be paid on every payday, not quarterly

Under Payday Super, you must pay your employees’ super guarantee at the same time as their salary and wages, for every pay run. The ATO is also updating SuperStream to improve error messages and introduce a new member verification request that helps reduce payment errors. Single Touch Payroll will also be updated to require employers to report both super liability and qualifying earnings for each pay run.

The 7-day rule: when your employees’ super fund must receive each payment

To avoid penalties, your employees’ super fund must receive their super payment within 7 business days after each payday. Sending the payment on payday is not the same as it being received. You need to allow time for processing by your clearing house or payroll provider. Check with your provider now to confirm how long their processing takes so payments can arrive within the 7-day window.

How Payday Super affects your cash flow and payroll processes in July

The move to more frequent payments will affect your cash flow and payroll processes. July 2026 in particular requires careful planning, as you may need to make multiple super payments at the same time, including:

- the final quarterly super payment for April to June 2026, due by 28 July 2026

- super payments for each payday from 1 July 2026 onwards

What you need to do before 1 July 2026

To be ready for Payday Super, employers should:

- Review your business and payroll processes to make sure you can pay super for each payday, or on the day you pay an invoice for contractors

- Make a plan for managing multiple super payments in July

- Check that your current super payments are going through correctly and that any changes to employee super fund details have been updated

ATO resources to help you prepare for Payday Super

The ATO has a range of resources to help employers prepare:

- Payday Super checklist for employers: a step-by-step guide on what to do and when

- Payday Super resources: videos, fact sheets and further guidance

- Payday Super main page: full information on the changes

If you have questions about how Payday Super will affect your business, get in touch with us.

Personal Risk Insurance Premiums Are Rising: Here’s Why

Personal risk insurance premiums have been rising across all major cover types, including life cover, total and permanent disability (TPD), trauma and income protection. There is no single cause. Several factors are working together to push costs up, and right now all of them are moving in the same direction.

Life insurance pricing reflects claims experience, distribution capacity, capital pressures and the investment environment insurers operate in. Cost of living is just one small part of the picture.

- Surge in mental health claims is pushing up TPD and income protection costs

The most significant driver is the rise in mental health related claims, particularly within TPD and income protection. Mental health is now the leading cause of TPD claims in parts of the market. Insurers are paying out billions annually in benefits linked to mental ill health, and there has been a marked increase in claims among younger Australians.

These are not small or short-lived payments. TPD benefits are designed to provide substantial financial relief when a person can no longer work, and income protection claims can run for long durations while a claimant is unable to earn.

In a pooled insurance system, when claim frequency rises, durations lengthen or claim sizes increase, insurers must reprice to ensure they can continue meeting obligations to all policyholders. That repricing flows through as premium increases, particularly where claims experience has deteriorated over multiple years.

- Decline in financial adviser numbers is increasing the cost of risk insurance

There are fewer financial advisers distributing personal risk insurance than there were at the peak of the late 2010s. Industry data based on the ASIC Financial Adviser Register shows the adviser population fell significantly from that peak and has stabilised at materially lower levels.

Risk advice is labour intensive. Fact finding, underwriting support, evidence collection, policy structuring and claims assistance all require time and specialist skill. With fewer advisers in the market, the cost to service each policy rises and access pathways narrow, adding friction and expense across the broader system.

- Insurer profitability problems in disability income insurance

Sustained profitability pressure in individual disability income insurance (IDII), which underpins many income protection products, is a third significant driver. APRA has been explicit about the scale of the problem, noting industry IDII losses in excess of $3 billion over a five-year period, even after significant premium increases had already been applied.

APRA also pointed to competitive dynamics that delayed product redesign, alongside higher claims, reserve strengthening and governance and data challenges.

When profitability is weak, insurers respond by tightening underwriting, reshaping products, strengthening reserves and repricing premiums to align expected claims costs with the capital required to support long-duration risks.

- Lower investment returns reduced the buffer insurers relied on to offset claims costs

Life insurers do not simply collect premiums and pay claims. They invest reserves and capital, and the returns on those investments have historically helped absorb underwriting volatility. A prolonged low interest rate environment compressed yields on high-quality fixed income, reducing the investment income that once provided that buffer.

When investment income is less reliable, the industry leans more heavily on underwriting adequacy, which feeds directly into premium pressure. Even as interest rates have moved, the transition has been volatile, with changes in discount rates and asset valuations affecting reported outcomes for institutions managing long-dated obligations.

How these factors are combining to push premiums up

What makes the current premium environment feel persistent is that these four drivers compound each other. Higher mental health claims lift the cost base. Fewer advisers reduce distribution capacity and increase unit costs. Weak profitability forces repricing and product redesign. Reduced investment income removes the cushion that once absorbed some of the strain. None of this stems from a single event. It is a system adjusting to new claims patterns and economic pressures.

If you would like to review your personal risk insurance arrangements, get in touch with us.

Will the New Anti-Money Laundering Rules Affect You from 1 July 2026?

From 1 July 2026, accountants, lawyers, real estate agents and other professional service providers are coming under Australia’s anti-money laundering and counter-terrorism financing (AML/CTF) laws. These rules already apply to banks and financial institutions, and they are now being extended to what AUSTRAC calls “gatekeeper professions.”

What is changing from 1 July 2026

The new rules are a legal requirement, not a policy choice. AUSTRAC, the Australian Government agency responsible for detecting and disrupting financial crime, now regulates accounting practices in the same way it regulates banks. The penalties for non-compliance are significant.

For you, this means that when we provide certain services we will need to verify your identity, understand the purpose of the engagement and assess any money laundering or terrorism financing risks. You may be asked to provide identification documents, confirm ownership details and, in some cases, provide information about where your funds are coming from.

Which services are covered by the new rules

The new rules apply to specific services known as “designated services.” For accountants, these include setting up companies, trusts and SMSFs, preparing trust deeds, restructuring entities, assisting with property transactions, holding or managing your funds in connection with a transaction, acting as a nominee director or shareholder, and providing a registered office address.

The majority of regular accounting work, including tax returns, BAS, bookkeeping, payroll, financial statements and general advisory, is not covered by the new rules.

What you need to know before 1 July 2026

The new rules apply to every accounting practice in Australia, so the checks are standard rather than something specific to your situation. If you would like to get ahead of the process, the most useful thing you can do is make sure your photo ID is current and your contact details are up to date.

We have prepared a Plain English Guide that walks through what is changing, which services are affected, what documents you may need and how the process will work in practice.

Download the AML Plain English Guide

If you have any questions about how the new AML rules apply to your situation, get in touch with us.

Renting Out Your Holiday Home? New ATO Rules Could Deny Your Deductions

This tax time, the ATO is expected to pay close attention to deductions claimed for holiday homes that are also listed for short-term rental through online accommodation platforms, particularly those not held mainly for earning rental income. The focus follows the release of new draft guidance from the ATO.

Why holiday home deductions are on the ATO’s radar

For several years there has been growing concern about individuals incorrectly claiming deductions. The National Tax and Accountants’ Association (NTAA) has flagged that the ATO’s focus this year will include holiday homes that appear to be held more for owner use than genuine rental purposes.

The two situations the ATO is most concerned about

The ATO has identified two situations where deductions are most often claimed incorrectly:

- The property is vacant and listed for rent, but the owner imposes unreasonable conditions such as excessive rent, requirements for references on short stays, or fails to follow up on genuine enquiries

- The property is listed for rent during off-peak periods but used by the owners during peak periods such as the December and January school holidays and Easter

In both situations, the property may technically be available for rent, but the way it is managed shows it is not genuinely held for earning rental income.

How the new ATO guidance changes what you can claim on a holiday home

The ATO has released two draft documents, TR 2025/D1 and PCG 2025/D7, which outline a new approach to assessing holiday home deductions. The guidance signals that if a holiday home is not mainly used for rental during the year, expenses related to ownership and use of the property will not be deductible under section 26-50 of the Income Tax Assessment Act 1997. This applies even where the property is actually rented to holidaymakers during the year.

The expenses that may no longer be deductible include:

- Mortgage interest

- Council rates

- Building insurance

- Land tax

- Repairs and maintenance

What counts as a leisure facility under the new rules

Section 26-50 denies a deduction for a loss or outgoing related to the ownership, use, maintenance or repair of a leisure facility. A leisure facility is defined as land, a building, or part of a building or other structure that is used or held for use for holidays or recreation. Under this definition, a holiday home used at any time by its owners for holidays or recreation falls within the scope of section 26-50.

Which holiday homes are most likely to attract an audit

Based on the new ATO guidance, section 26-50 is most likely to apply to holiday homes blocked out or reserved for owner use during most or all of the peak periods. These are the properties the ATO will be paying closest attention to this tax time. If your property is mainly used by you and your family during peak rental periods, with limited genuine availability during those times, your deductions are at higher risk of being denied.

Are you claiming the right deductions on your holiday home?

The new draft guidance tightens the rules around what qualifies as a genuine rental property. If you own a holiday home that is also rented out and want to make sure your deductions are properly claimed, get in touch with us.

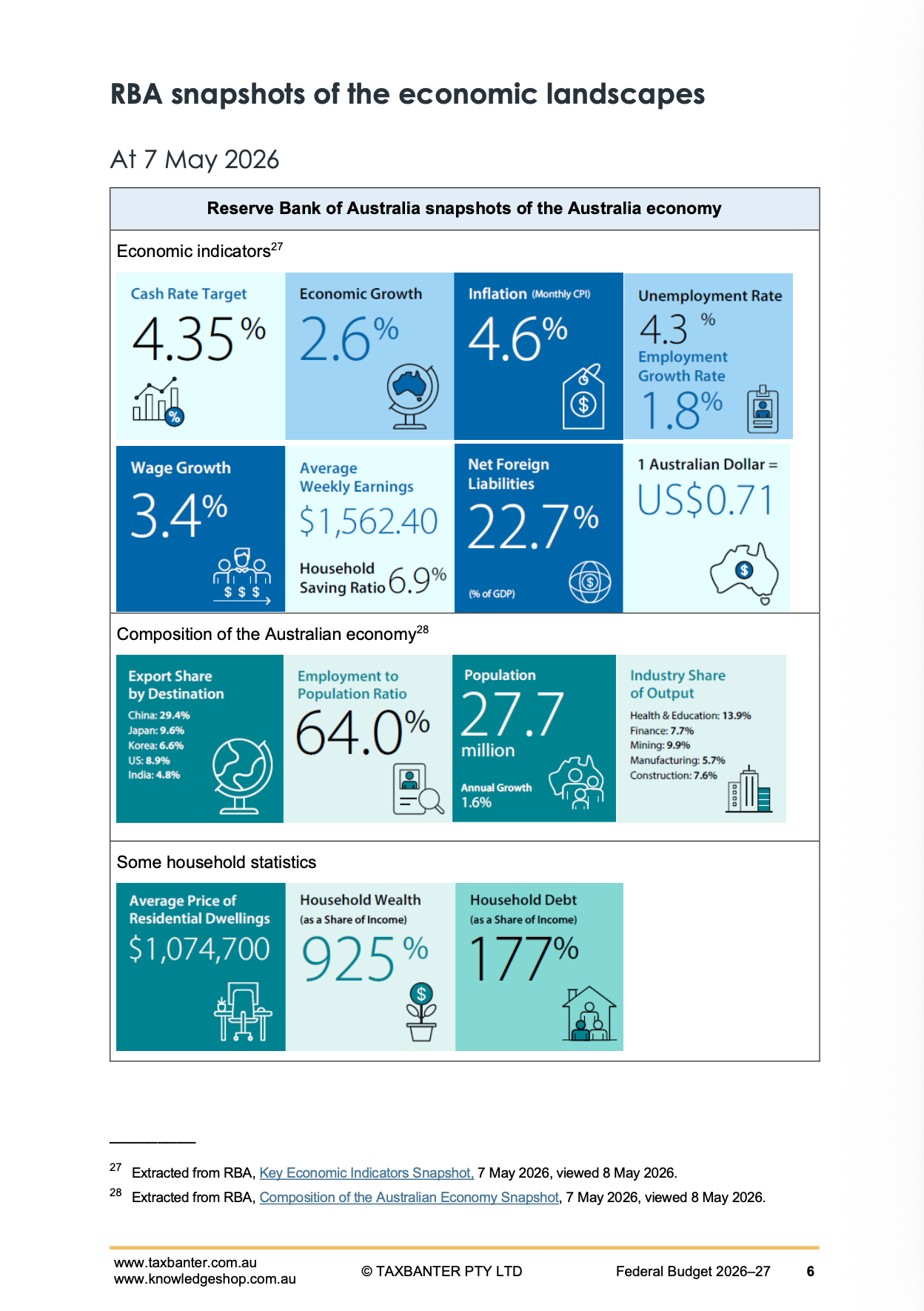

2026-27 Federal Budget: The Changes Most Likely to Affect You

We’ve reviewed the 2026-27 Federal Budget and identified the changes most likely to affect you. None of these measures are law yet, but some require action sooner than you might think. If any of the following apply, it’s worth talking to us now:

- Hold investments or business assets you plan to sell, including shares, property or goodwill

- Distribute income through a discretionary (family) trust

- Own a negatively geared investment property purchased after 12 May 2026

- Are a small business owner with equipment purchases planned

- Run a company that has made or expects to make a tax loss

If you hold investments or business assets you plan to sell (shares, property, goodwill), it’s proposed that the 50% CGT discount will be replaced with indexation and a 30% minimum tax from 1 July 2027

The Government has proposed replacing the current 50% CGT discount with inflation-adjusted indexation and a minimum tax rate of 30% on realised gains from 1 July 2027. The change would apply to all CGT assets held by individuals, trusts and partnerships for more than 12 months. The CGT net will also be broadened to include pre-1985 assets for disposals from that date.

What this means for you

If you’re planning to sell a business, property or investment asset, gains realised before 1 July 2027 will still be taxed under the current 50% discount rules. After that date, the discount disappears and a minimum 30% tax rate applies on your real gain. Depending on the size of your gain and how long you’ve held the asset, selling before 1 July 2027 could result in a meaningfully lower tax bill.

There is also a practical step worth understanding now. Any asset you hold before 30 June 2027 that you plan to keep beyond 1 July 2027 will need to be valued at 30 June 2027. That valuation locks in the gain that qualifies for the 50% discount up to that date. From 1 July 2027, indexation applies to any further gain. Without a valuation at 30 June 2027, working out the split between the two regimes when you eventually sell becomes much harder.

There are also some important exceptions to be aware of:

- If you hold assets in an SMSF, the CGT discount percentage of 33.33% is expected to continue

- If you’re eligible for small business CGT concessions, these remain in place

- If you’re buying a new residential property as an investment, you’ll be able to choose between the 50% discount and indexation with the minimum tax when you sell

- If you receive an income support payment including the Age Pension, you’ll be exempt from the minimum tax

This is worth a conversation with us before you make any decisions about selling.

If you distribute income through a discretionary (family) trust, discretionary trusts may face a 30% minimum tax on income from 1 July 2028

From 1 July 2028, trustees of discretionary trusts would pay a minimum tax of 30% on the taxable income of the trust. Beneficiaries, other than corporate beneficiaries, would receive non-refundable credits for the tax payable by the trustee.

What this means for you

If you currently distribute trust income to beneficiaries on lower marginal tax rates, the strategy may no longer deliver the same outcome. The 30% marginal rate currently applies to taxable income between $45,000 and $135,000, so beneficiaries with taxable income below $45,000 would end up paying a higher rate of tax on their trust distribution than on the rest of their income.

There are also some important exceptions to be aware of:

- Fixed and widely held trusts, complying super funds, special disability trusts, deceased estates and charitable trusts are not affected

- Primary production income, certain income relating to vulnerable minors, amounts subject to non-resident withholding tax, and income from assets of discretionary testamentary trusts existing at the time of the announcement are also excluded

- The Government has flagged expanded rollover relief for three years from 1 July 2027 to support those who wish to restructure out of discretionary trusts into another entity type

If you’re a trust beneficiary or trustee, it’s worth reviewing your structure now to understand your options.

If you own a negatively geared investment property purchased after 12 May 2026, losses will only be deductible against residential property income from 1 July 2027

From 1 July 2027, losses from established residential properties would only be deductible against rental income or capital gains from residential properties. Excess losses would be carried forward and could be offset against residential property income in future years.

What this means for you

If you purchased an established residential investment property after 7.30pm AEST on 12 May 2026, you would no longer be able to offset rental losses against your salary or other income from 1 July 2027. The deduction is still available, but only against income from residential property.

There are also some important exceptions to be aware of:

- Residential properties owned at the time of the Budget announcement on 12 May 2026 are not affected

- Eligible new builds of residential premises are excluded

- Properties held in widely held trusts and superannuation funds, including build-to-rent developments, are excluded

- There is no limit on the number of properties you can negatively gear under the new rules, provided they fall within the exclusions or generate offsetting residential property income

If you’re considering an established residential investment property purchase, the timing and structure are worth discussing with us first.

If you are a small business owner with equipment purchases planned, the $20,000 instant asset write-off is now permanent

The Government has permanently extended the $20,000 instant asset write-off for small businesses with a turnover of up to $10 million. The threshold had been set to expire on 30 June 2026 and revert to $1,000.

What this means for you

You now have certainty over asset purchase planning going forward. Eligible assets costing less than $20,000 can be written off in full in the year they are first used or installed ready for use.

Two further points to be aware of:

- Assets valued $20,000 or more can continue to be allocated to the small business simplified depreciation pool, with deductions of 15% in the first year and 30% in later years

- The rule that prevents small businesses from re-entering the simplified depreciation regime for five years after opting out will continue to be suspended until 30 June 2027

If you’re planning major equipment purchases, get in touch with us to map out the timing.

If you run a company that has made or expects to make a tax loss, the loss carry-back regime returns from 1 July 2026

From 1 July 2026, companies with aggregated annual global turnover of less than $1 billion will be able to carry back a tax loss and offset it against tax paid up to two years earlier. The measure applies to revenue losses only and is limited by a company’s franking account balance.

What this means for you

If your company has paid tax in the past two years and now has a revenue loss, you may be able to claim back some of that tax rather than carry the loss forward. The Government estimates the measure will directly benefit up to 85,000 companies each year.

If your company is in a loss position or expects to be, it’s worth talking to us about whether the loss carry-back applies to your situation.

If you would like to talk through how any of the 2026-27 Federal Budget changes apply to your situation, get in touch with us.

Important: This is not advice. Clients should not act solely on the basis of the material contained in this article. Items herein are general comments only and do not constitute or convey advice per se. Also changes in legislation may occur quickly. We therefore recommend that our formal advice be sought before acting in any of the areas. This article is issued as a helpful guide to clients and for their private information. Therefore it should be regarded as confidential and not be made available to any person without our prior approval. Liability limited by a scheme approved under Professional Standards Legislation.