February 2026 Round Up

This month we focus on three areas where common financial structures and systems can create risk if they are not aligned with how the rules operate in practice. From trust distributions that appear standard on paper but raise questions about who actually benefits, to payroll systems that must adapt to Payday Super from 1 July 2026, routine arrangements still need to operate in line with how the rules work in practice.

We also step back from compliance to look at financial capability at a different level, exploring how parents and grandparents can approach teaching children about money in practical, age appropriate ways. Read more below.

1. Payday Super Readiness: Is your payroll system ready? Read the full article

2. How a “Standard” Family Trust Setup Led to a Costly ATO Section 100A Review Read the full article

3. How to Help Your Kids Become Money Savvy, One Age-Appropriate Step at a Time Read the full article

Payday Super: preparing your payroll system for July

From 1 July 2026, super will be paid at the same time as salary and wages rather than quarterly. This means payroll systems will need to calculate and process super contributions as part of each pay cycle, instead of relying on end-of-quarter processing.

For many businesses, this will involve a shift from end-of-quarter processing to automated super payments as part of each pay run. If pay items or super settings are not configured correctly, issues may repeat each cycle rather than sitting unnoticed until quarter end.

This doesn’t change how much super is owed. It changes how consistently payroll systems need to apply it.

With July approaching, understanding how super is currently configured within your payroll system can help ensure it operates smoothly once the new rules begin.

If you would like help reviewing your payroll setup or preparing for Payday Super, please get in touch — we’re here to help.

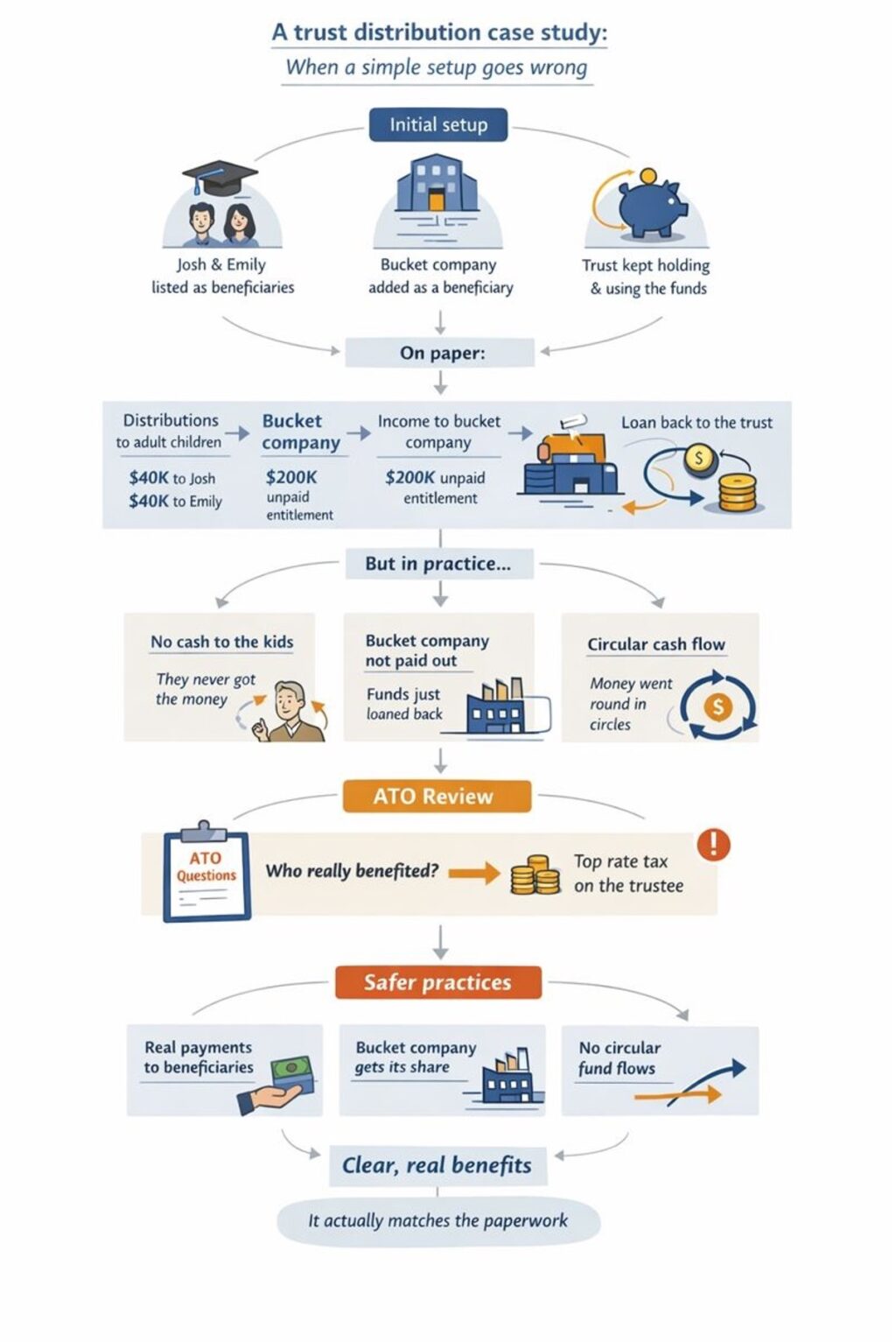

How a “Standard” Family Trust Setup Led to a Costly ATO Section 100A Review

Most family trusts in Australia are set up in a similar way. Income is distributed on paper to adult children or bucket companies to manage tax, while the money often stays in the family business for everyday use.

Because this approach is so common, many families assume it is perfectly safe. But that is not always the case.

This real example shows how a standard discretionary trust setup led to an ATO Section 100A review, several years of trust distributions being treated as ineffective for tax purposes, and an unexpected tax bill for the trustee, even though tax had already been paid by the named beneficiaries.

The Background

Mark and Lisa ran a successful family business through what most people would describe as a fairly standard discretionary trust. The trust was established when the business was small and cash was tight. Over time, the business grew, profits improved, and the trust began distributing larger amounts of income each year.

The tax returns were lodged. There had never been a problem with the ATO. On the surface, everything looked to be in order. Years later, the ATO took a different view

Year one: the seemingly ‘normal’ distribution that created a bigger problem later

In a strong year, the business earned about $280,000.

To manage tax, the trust distributed $40,000 each to Mark and Lisa’s adult children. Both were over 18, both were studying, and neither earned much income. The remainder was split between Mark, Lisa, and a company beneficiary.

On paper, the tax outcome improved.

However, no money was ever paid to the children. There were no bank transfers, no separate accounts, and no decisions made by the children about how the funds should be used. Instead, the trust retained the money in its main business account to pay suppliers and reduce debt.

At the time, this was viewed as “family money” that could be accessed later.

That single detail – that the children never actually received or controlled the distributions – became critical years later.

Year two: a tidy company structure that didn’t change who benefited

The following year was even stronger. The trust continued to use a bucket company to cap tax at the company rate, a common and legitimate strategy when structured and implemented correctly.

The trust distributed $200,000 to the company as an unpaid present entitlement, with the intention it would be paid when cash flow allowed.

In practice, the trust effectively borrowed the funds back from the company, with balances managed through loan arrangements and year-end accounting entries. The company did not use the funds for its own business or investments, and economically, nothing had changed.

Year three: when routine distributions kept the benefit in the same hands

By the third year, the process had become routine.

Distributions were again made to the children. The company received another entitlement. Loans were adjusted through year-end journal entries.

What this created was a circular flow. Income was allocated on paper, but the money either never left the trust or returned almost immediately through loans or offsets.

No single step appeared problematic in isolation. Together, however, the pattern reinforced the same issue: the economic benefit of the trust income consistently remained with the same people.

The ATO review: when trust paperwork and cash flow don’t align

Mark later received a letter from the ATO. It was not an audit notice. It was described as a review.

The ATO asked for:

- the trust deed

- distribution resolutions

- loan agreements

- bank statements

- explanations of how beneficiaries benefited from distributions

Josh and Emily were asked whether they received the trust distributions, whether they knew about them, and whether they decided what to do with the money.

They said they did not really think about it, their parents handled it, and they did not receive the cash.

The ATO’s focus: who actually benefited from the trust income

The ATO did not argue that the trust deed was invalid, that the resolutions were late, or that tax returns were lodged incorrectly.

Instead, they focused on one question: who actually benefited from the trust income?

The ATO view was that:

- the adult children were beneficiaries on paper only

- the bucket company never truly benefited

- the trust controllers enjoyed the economic benefit

- the arrangements were not ordinary family dealings

This brought the arrangement within the scope of section 100A.

The result: trust distributions ignored and tax shifted to the trustee

The ATO proposed to treat several years of trust distributions as ineffective for tax purposes and assessed the trustee at the top marginal tax rate on those amounts.

This occurred even though tax had already been paid by the children and the company.

While refunds may be possible in some circumstances, the immediate impact was a significant and unexpected cash-flow burden for the trustee.

What could have reduced the risk

None of the decisions in this example were extreme or unusual.

However, a few changes would have significantly reduced the risk.

If the adult children had actually received the distributions and controlled how the money was used, the arrangement would have been far stronger. That does not prevent parents from helping later, but the benefit needs to sit with the beneficiary first.

Similarly, if the company beneficiary had used the funds for its own investments or working capital, rather than acting as a temporary holding point, the outcome may have been different. A company beneficiary needs to operate as a real entity, not just exist for tax outcomes.

Trustees should also feel comfortable stepping back each year and asking simple questions:

- Who is really benefiting from this distribution?

- Will the money actually be paid?

- Would this arrangement still make sense if tax was not a factor?

These questions often highlight issues early, when they are far easier to address.

What this means in practice

Section 100A is not concerned with intent or wrongdoing. It looks at what actually happened in practice.

Where trust income is allocated to one party, but the economic benefit sits elsewhere, the ATO may step in and rewrite the tax outcome.

This is why alignment between trust paperwork and how money is actually used matters over time, particularly where arrangements continue year after year.

How to Help Your Kids Become Money Savvy, One Age-Appropriate Step at a Time

Financial literacy is one of those life skills that rarely gets taught in the classroom, which means the responsibility often falls to parents and grandparents. But where do you start if you want to give your kids or grandkids the best chance of financial success?

The good news is that you don’t need a finance degree to do it well. You simply need to start with simple conversations and build on what your child can understand at each stage.

Here is a practical breakdown of what to focus on and when.

Primary school (ages 6 – 12): Show them what money is

Before children can learn to manage money, they need to understand what it actually is. At this age, that means making it something they can see, hold, and make decisions about.

A small, regular allowance is one of the simplest ways to show children that money is limited. It does not appear automatically, and once it is spent, it is gone. That single concept is the foundation everything else builds on.

From there, simple choices start to teach bigger ideas. Spending now or saving for something bigger introduces patience, trade-offs, and planning without any need for a lecture. The child experiences what money is by using it.

Making money visible reinforces this. Clear jars or piggy banks let children watch their savings grow, connecting the act of waiting with a visible reward. Some families separate money into jars for spending, saving, and sharing, which shows children that money serves different purposes.

Small mistakes matter here too. If a child spends their allowance too quickly and feels the regret later, that is a low-stakes lesson in what money is and what it is not. It is not unlimited, and it does not come back once it is gone. This is the first step in helping children become confident with money.

Secondary school (ages 12-18): Show them what money does

As children move into their teenage years, money stops being theoretical. This is when everyday financial systems start to affect them directly.

Opening a bank account together helps show how money is stored, accessed, and tracked. Teenagers can also begin to understand that banks are businesses — they pay interest on savings but charge much higher interest on borrowed money.

Using a debit card introduces responsibility without the risks that come with credit. Tracking balances and spending through apps helps connect decisions to outcomes.

This is also the stage where trade‑offs become more visible. Comparing needs and wants, and contributing toward higher‑cost items, reinforces the idea that spending choices have consequences.

For teenagers earning income, checking pay rates and understanding entitlements builds confidence and awareness. It also introduces the habit of reviewing information rather than assuming it is correct.

Saving at this stage is less about amounts and more about behaviour. Setting money aside as soon as it is earned helps establish the habit of prioritising saving rather than relying on what is left over.

School leavers (ages 18+): Show them what money can become

When young adults enter full‑time work or further study, their financial decisions begin to have longer‑term effects.

Understanding superannuation early gives young adults context for how long‑term saving works. Even small contributions benefit from time and compound growth, making early awareness more valuable than large contributions later.

Exposure to investing should be cautious and grounded. Digital investing platforms make access easier, but the underlying principles still matter. Higher potential returns come with higher risk, and diversification reduces the impact of individual losses.

At this stage, the focus is not on picking investments but on understanding how markets behave and why spreading risk matters.

What this means in practice

Teaching children about money is rarely about one big lesson. It is about repeated, ordinary decisions and conversations that shape how money is viewed and used over time.

Simple, consistent approaches — allowances, saving habits, understanding pay, and early exposure to long‑term concepts like super, investments, and compounding interest — tend to have more impact than complex strategies introduced later.

For parents and grandparents, the key is not knowing everything, but setting up real life examples where knowledge is gained through safe and age-appropriate experiences.

Important: This is not advice. Clients should not act solely on the basis of the material contained in this article. Items herein are general comments only and do not constitute or convey advice per se. Also changes in legislation may occur quickly. We therefore recommend that our formal advice be sought before acting in any of the areas. This article is issued as a helpful guide to clients and for their private information. Therefore it should be regarded as confidential and not be made available to any person without our prior approval. Liability limited by a scheme approved under Professional Standards Legislation.